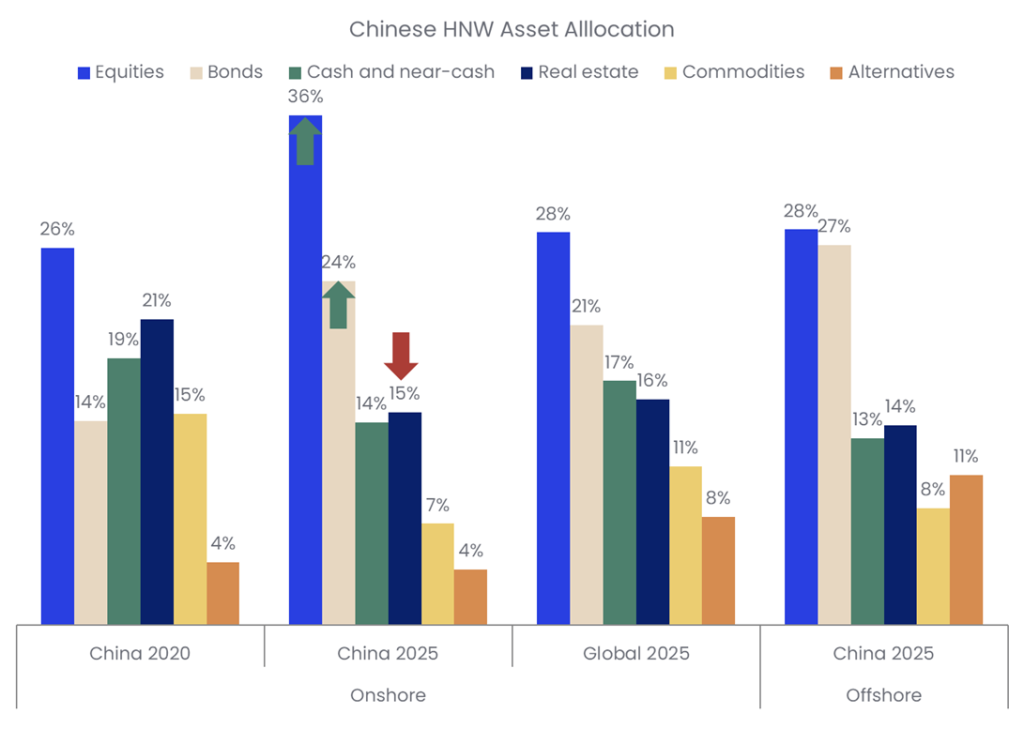

Chinese HNW portfolios show a decisive rotation away from real estate, with allocations falling from 21.4% in 2020 to 14.9% in 2025. This is not cyclical. Property has historically acted as the default store of value, but ongoing developer stress, weak liquidity, and policy intervention have shattered confidence.

GlobalData Global Wealth Managers Surveys

As mainland investors are abandoning real estate, wealth is being redeployed rather than held in cash. Data from our Global Wealth Managers Surveys (2020 and 2025) shows that the proportion of Chinese HNW onshore wealth allocated to equities has risen sharply and now sits well above the global average—a strong reversal from the historic trend.

Recent performance has supported this shift, with Chinese equities delivering strong gains over the past year. In 2025, the MSCI China returned 29.8%, compared to the MSCI World 15.6% (both USD gross total return).

However, this shift is unlikely to be permanent. The rally has been policy-driven and volatile. Going forward, we expect higher volatility to drive demand for income generation and capital preservation, not typically equity’s strong suit in times of global economic stress.

In fact, fixed income has already increased materially from 14.3% in 2020 to 24.1% in 2025. This is a significant reweighting, and fixed income is no longer a residual allocation; it is becoming a core component.

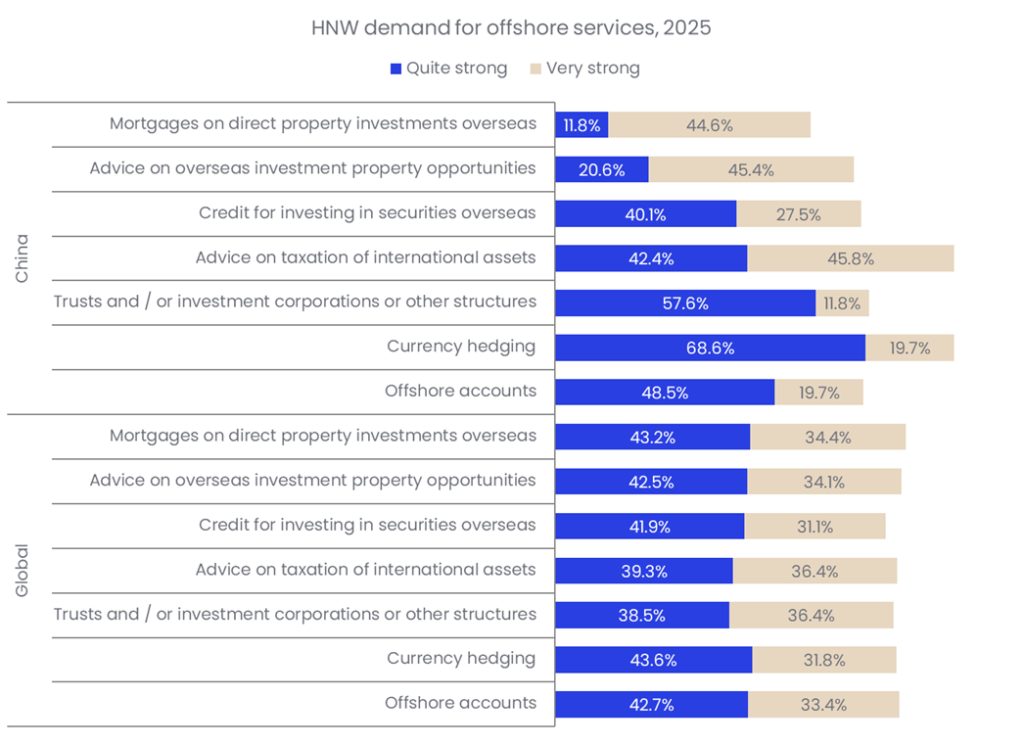

At the same time, we are seeing heightened demand for offshore structures as wealth locked up in property is freed up. 32% of Chinese HNW wealth is already booked abroad, primarily driven by access to broader investment opportunities. This trend is expected to accelerate, with a net 66% of private wealth managers anticipating further increases over the coming year.

Offshore portfolios: higher allocations to alternatives and bonds

This reinforces the shift towards diversification and income outside domestic markets.

This dual shift—away from property and towards both income assets and offshore exposure—provides wealth managers with a significant opportunity to demonstrate their utility.

Property historically required limited ongoing advice, and a substantial amount of HNW wealth was inaccessible to wealth managers. Now this is being replaced with a need for continuous allocation decisions across asset classes, currencies, and jurisdictions. Indeed, we have seen a move from advisory-led propositions to discretionary mandates, which now account for 39% of Chinese HNW wealth.

As portfolios are becoming more complex in an increasingly volatile environment, this enforces the need for scalable discretionary models. The focus should be on building income-oriented solutions. Demand will centre on fixed income, structured products, and multi-asset strategies that can deliver stable returns in a more volatile environment.

Secondly, developing robust offshore capabilities will be critical. Demand for offshore services is already strong, particularly in currency hedging, structuring solutions, and offshore accounts. Access to Hong Kong (China SAR) as well as other booking centers, integrated onshore-offshore platforms, and cross-border structuring expertise will be critical differentiators. Clients are not simply allocating offshore, they are doing so in more complex, structured ways.

Opportunities for new brands, international outfits

The key implication is that Chinese HNW wealth is becoming more mobile, more diversified, and significantly more accessible to active portfolio management. Those wealth managers that remain positioned around transactional, property-linked models along with ill-sold wealth management products will lose relevance as wealth shifts into managed and internationally diversified portfolios that have not featured prominently in the mainland wealth management market previously. This is a distinct opening for new brands and international players looking to build a presence among affluent mainlanders.

Heike van den Hoevel is Principal Analyst, Wealth Management, GlobalData